Delhi: India’s smartphone market will end the year 2021 with a low single-digit annual growth as per IDC data.

As per IDC Worldwide Quarterly Mobile Phone Tracker data, India’s smartphone market recorded a 12% year-over-year (YoY) decline in 3Q21 (Jul-Sep). Around 48 million smartphone units were shipped in 3Q21, which are lesser compared to four consecutive quarters of growth.

Component shortages and an unusually high 3Q20 comparison base (whereas this year’s post-lockdown demand was addressed by July) resulted in lesser shipments. Compared to 3Q19, 3Q21 grew by 3% as channels stocked up for the Diwali quarter amid the supply shortages.

“The first nine months of the year (Jan-Sep’21) already shipped 120 million units, with first half of 2021 clocking 42% YoY growth. Due to supply challenges, 4Q21 is expected to see a decline, resulting in annual shipments below 160 million in 2021,” said Navkendar Singh, Research Director, Client Devices & IPDS – IDC India.

“The first half of 2022 will remain challenging, with some easing out expected in the latter half of 2022. Vendors/channels will keep an eye on the over-stocking situation in case demand stays limited due to the price hikes by the suppliers and vendors,” added Singh.

Key market trends for 3Q21 included:

- Online channels clocked a record high 52% share, although with a 5% YoY shipment volume decline. eTailer sales festivals (The Big Billion Days on Flipkart and Amazon Great India festival) started in early October, even before the Navratri festival this year, continuing until Diwali. Offline channels registered an 18% YoY shipment decline. IDC expects online shipments to surpass offline shipments in 2021.

- India was the third-largest 5G smartphone market globally with 7% of worldwide 5G shipments, shipping 10 million units at an ASP of $401 in 3Q21. From Jan-Sep’21, 17 million 5G smartphones were shipped to India and are expected to be under 30 million for 2021. The OnePlus Nord CE, iPhone 12, and Galaxy A22 were the most popular 5G models in 3Q21.

- Overall ASPs peaked at $196, driven by price hikes and a greater 5G contribution. The sub $200 segments dropped by 24%, while $200+ smartphones grew by 56%, signalling a shift to higher price buckets, driven primarily by supply.

“IDC believes that a growing dependency on smartphones triggered by remote work and learning, as well as a subsequent requirement for better quality hardware is pushing consumers to spend more. With continued chip shortages and logistics costs, brands are also compelled to expand upwards in terms of price points across channels,” said Upasana Joshi, Research Manager, Client Devices, IDC India.

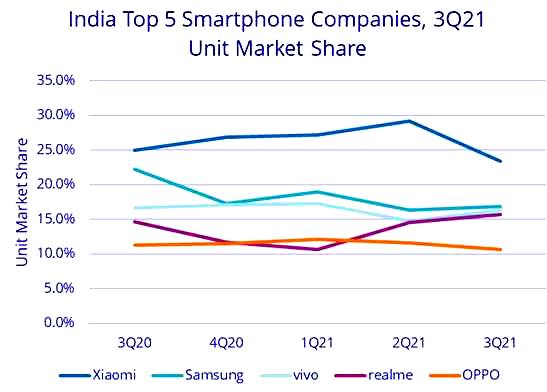

Top 5 Smartphone vendor highlights in India’s smartphone market

Xiaomi continued to lead but shipments declined by 17% YoY. Poco, Xiaomi’s sub-brand exclusive to the online channel, witnessed high 65% YoY growth. 72% of Xiaomi’s shipments were concentrated in the online channel, with its market share there dropping to 32%. The Redmi 9A/9 Power/9/Note10s were the major volume drivers along with the Poco M3 and Poco C3.

Samsung, at the second slot, registered the highest YoY decline amongst the top 5 vendors at -33% in 3Q21. With a key focus on the Galaxy M and F series, 49% of its shipments were sold online, allowing the vendor to take 16% of all online shipments. However, offline models like the Galaxy A22/A12 accounted for 23% of the vendor’s overall shipments. The opening quarter for the Galaxy Z Fold3 and Z Flip3 witnessed a demand surge but had supply constraints. Samsung stood at a leadership position within the 5G segment with its new model offerings.

vivo was at the third position, with a 13% YoY shipment decline. It continued to cement its offline presence with a 30% share of that segment. Also, it strengthened its portfolio in the $200-300 segment with its V and iQOO series as well as its marketing campaigns for the X series.

realme at the fourth slot had the best performance of the top 5 vendors with a 5% YoY decline. In the online space, it continued to be at second slot ahead of Samsung with a high 22% share. However, within the 5G segment, it slipped to the third slot. The C11 (2021) and realme 8 (which includes both the 4G/5G models) were the highest shipped devices.

OPPO, at the fifth slot, witnessed a 16% YoY decline in 3Q21. However, in the $300-500 segment, OPPO rose to the second slot with an 18% share, driven by high shipments for the Reno 6 series. Also, it slipped to the third slot in the offline channel with a 17% share there.